- About Us

- Climate & Environment

- Our Culture

- Governance

- Stories

Chubb Group Executives

Chubb has operations in 54 countries and territories and can help clients manage their risks anywhere in the world.

The company took its present form in 2016 when ACE Limited acquired the Chubb Corporation, creating a world leader in insurance.

The National Geographic Society and the Chubb Charitable Foundation are partnering together to drive transformational change for vital ecosystems at the intersection of land and water.

Chubb Climate+ draws on our extensive technical capabilities in underwriting and risk engineering, bringing together Chubb units engaged in Renewables, Alternative Fuels, Climate Tech, and Risk Engineering services.

At Chubb, we recognize our responsibility to provide solutions that help clients manage environmental risks, to reduce our own environmental impact and to make meaningful contributions to environmental causes.

Chubb’s culture is defined by who we are, the behaviors we expect of each other, and what we reward and recognize.

Guided by steady leadership and a commitment to the highest levels of personal and professional integrity.

Discover our latest news, insights, stories and profiles

Unique proposal recognizes that pandemics affect small and large businesses differently.

The devastating impact of COVID-19 on businesses and employees prompted policymakers and insurance industry leaders to look for a better way to provide effective and timely assistance to businesses in the event of a future pandemic.

Chubb emerged as a leader in this policy discussion with the release of its Pandemic Business Interruption Program, which proposes a public-private partnership that would provide financial support for businesses if a pandemic again shuts down the economy.

The Chubb plan has two core elements: a program for small businesses that provides an immediate cash infusion when a pandemic is declared; and a separate voluntary program for medium and large businesses.

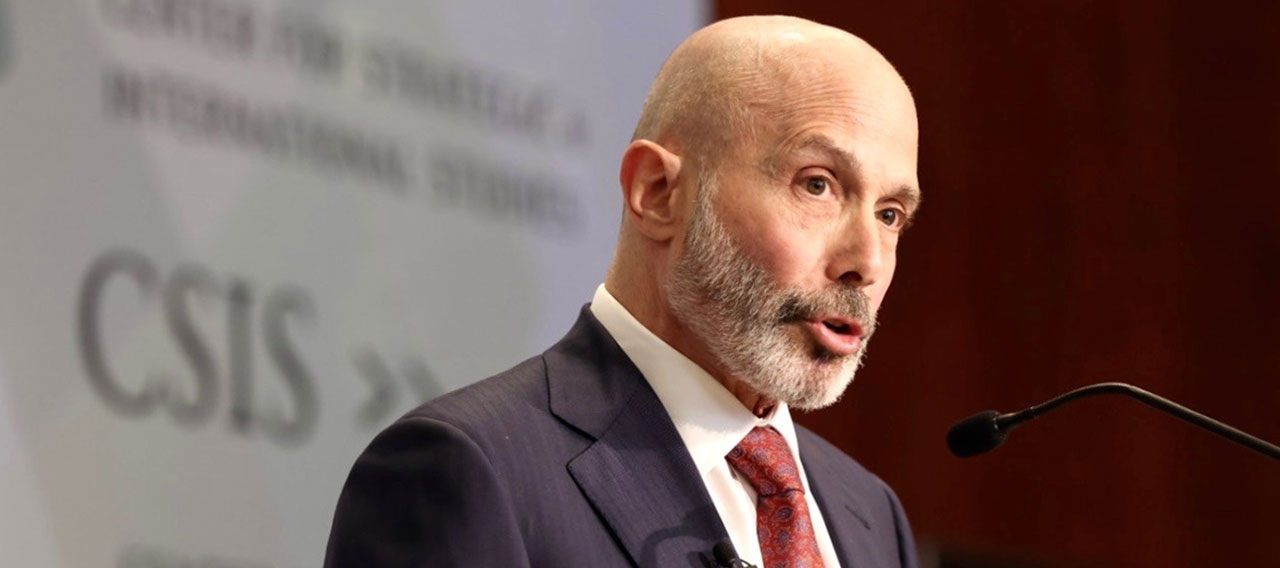

Evan Greenberg, Chubb Chairman and CEO, testified about the plan at a U.S. Senate hearing, “Examining Frameworks to Address Future Pandemic Risk,” hosted by the Committee on Banking, Housing & Urban Affairs’ Subcommittee on Securities, Insurance and Investment.

“We believe the insurance industry can play an important role in partnership with the federal government to blunt the economic impact of future pandemics by keeping businesses solvent and people employed,” Greenberg told Congress.

The purpose of the hearing was to assist Congress in deepening its understanding of various proposed frameworks to help businesses prepare for and weather the impacts of future pandemics. In addition to Greenberg’s testimony, committee members heard from a small business owner who was impacted by the pandemic, an academic expert on risk, the American Property & Casualty Insurance Association and the President of Marsh’s U.S. and Canadian business.

“Pandemics, unlike other catastrophes such as earthquakes, hurricanes, floods and even terrorism, are not limited to a specific geography, time period, or risk class, but instead can affect entire economies, almost every business, and most of the population at the same time, resulting in losses so great that the event is uninsurable by the insurance sector alone,” Greenberg said. “Congress sought to fill the gap by enacting assistance programs totaling trillions of dollars, including hundreds of billions of dollars for small businesses. While these programs have been largely successful, with businesses of all sizes securing loans and grants to stay afloat, the ad hoc nature of these well-intended relief efforts is not a formula for future success.”

Unique among the various proposals, the Chubb plan is structured in two parts: one for small businesses and a second approach for businesses with over 500 employees. The bifurcated approach recognizes that pandemics affect small and large businesses differently. Among the key elements of the plan:

- Affordability and certainty for small businesses about the amount of financial support available if a pandemic shuts down the economy

- Quick and efficient payment of a pre-determined sum to small businesses without the need to adjudicate individual claims

- An incentive to keep people employed, rather than relying on unemployment relief

- A market-oriented program for larger businesses intended to support and stimulate the private market for pandemic coverage

- Insurance industry risk-sharing with the federal government, together with a better understanding of pandemic risk, risk mitigation and preparedness, increasing over time

“We can be better prepared for the next pandemic by acting now to limit the health and economic consequences of such a catastrophe,” said Greenberg. “We also know what can be done to provide prompt financial support to keep businesses solvent and employees off the unemployment rolls. Combining the insurance industry’s risk insight and experience with the government’s balance sheet capability to take on pandemic tail risk provides the foundation for an affordable, efficient liquidity backstop for small businesses and a market-based program for larger businesses.”